This year’s AFC summer conference featured the first ever AFC Big Debate, sponsored by NETSOL Technologies, with two teams of experts arguing the pros and cons of mandatory commission disclosure and battling it out to win the votes of their audience.

Debate chair Jason Hurwitz, sales director Europe at NETSOL Technologies, explained the aim was to “flush out all sides of a real and tangible industry issue so they can be discussed without fear or favour.”

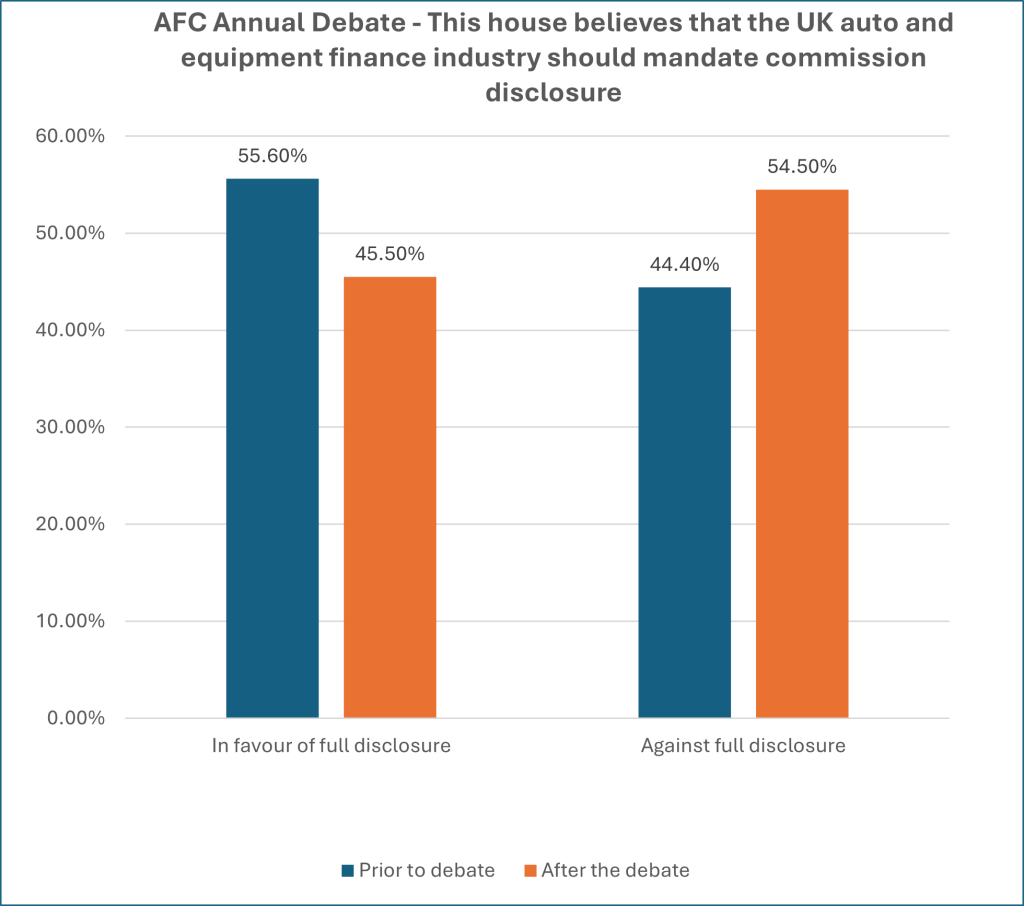

An initial poll via the AFC app found a narrow margin between the two opposing views, with 55.6% of the audience in favour of compulsory disclosure and 44.4% against. But as Hurwitz pointed out “make no mistake – it’s a competitive debate and the winner is the side which sways the audience views the most. The speakers are not allowed to sit on the fence”.

PETTS

First up was John Rees, AFC’s community head, equipment finance, speaking in favour of the motion. On what he labelled “a day of acronyms” Rees added one more: PETTS, which he described as “warm, cuddly and furry”.

The elements of PETTS are professionalism, which must be evident the whole time in all aspects of work, particularly with regard to the borrower understanding all the economics of a transaction, followed by being ethical in dealing with people’s ability to borrow and use that lending to buy assets.

Next comes transparency – how can customers be convinced they are receiving a value for money service if they are not aware of all the financial elements of a transaction?

That links directly to trust, with customers unable to trust the commercial relationship if there is not total transparency around commission.

“And most provocatively the final element is self regulation. We are a professional, transparent and ethical business. If we wait for the FCA to impose something on us, we don’t know what that will be, but we do know for sure it will never be changed. Therefore, it’s incumbent on us to control our own industry and self regulate,” Rees declared.

Full disclosure

Having stated “all I want you to do is think of your PETTS,” Rees gave the floor to David Betteley, AFC head of content, to advance the alternative point of view.

Betteley sought to clarify the grounds for debate, pointing out that commission disclosure for regulated agreements has been a principle for many years. The crucial point is around full commission disclosure, which means confirming not just the existence of any commission but also the actual amount.

“There have been lots of surveys about this, including by major dealer groups, and they’ve all found that the number of customers who ask about the amount paid is infinitesimally small. There isn’t any real interest from customers in finding out,” Betteley explained.

Instead, the customer typically has three concerns about any deal: the price of the goods, and the possibility of a discount; the part exchange allowance; and the size of the monthly payments.

“There are many examples where the customer negotiates a £2000 discount, and the commission paid is £1000. So, they are happy with the overall structure of the deal. The commission is important, but it’s not the deciding factor,” Betteley pointed out.

Many auto finance agreements are already very heavily regulated, with lenders and dealers required to provide information on the cost, deposit, balance to finance, fees, APR and monthly payments.

“But all the surveys show customers don’t use APR to compare and they don’t understand it. People under 25 have an even lower knowledge of APR than older people. I’d say there’s a definite comparison between the APR and the amount of commission – customers just don’t take it into account. They look at the overall deal,” Betteley argued.

And it’s the additional service from dealers which is typically priced into the package that customers seem to value, with online-only options such as Cazoo rejected in favour of an omnichannel approach.

Storybook lending

In the asset finance sector, brokers are dealing with clients with a wide range of credit ratings. Customers with a lower credit rating are more difficult to place with a lender and can require extra work if, for example, five years of accounts are required rather than one.

“You tell a story to the lender and that takes a lot of time, a lot of work and a lot of skill and it seems only fair to me that that is rewarded by payment of commission. I don’t think the amount of that commission is a deciding factor for consumers, and perhaps the concern lies more with the trade associations and the regulators,” Betteley declared.

He went on to caution about the unintended consequence of mandating full disclosure, which include fewer lenders in the market, meaning less choice for consumers, less competition, higher prices and – most significantly – more difficulty for people with lower credit ratings in obtaining credit.

“This results in increased risk aversion towards SMEs and entrepreneurs and risks stifling economic growth,” Betteley concluded.

Supporting arguments

Summing up the argument as being between “furry animals and regulatory creep”, Hurwitz introduced Wayne Gibbard, partner at Shoosmiths, to second Rees’ proposition. Agreeing that “transparency, trust integrity should be at heart of what we do and full disclosure is part of that”, Gibbard identified five key regulatory points which play a part in encouraging full disclosure.

These are Consumer Duty, which has introduced a higher degree of requirements around customer understanding; senior management’s requirement to demonstrate that decisions and actions have been made “in good faith”; the need to manage conflicts of interest; compliance with CONC, which already says if a customer asks about the amount of commission they should be told, so providing this proactively is an easy operation win; defeating claims management companies; and finally winning a competitive edge.

“The ability to be transparent with your customer and take a step forward before the regulator tells you means you are in control of your own destiny,” Gibbard stated.

On the other side, Finativ CEO Christian Roelofsidentified three problems in the debate’s content. Firstly, the sector embraces asset, auto and equipment finance, and the three cannot be “lumped together” when making decisions about commission disclosure.

Secondly, as he put it “we don’t even understand what commission or disclosure actually means enough to even consider an instrument such as full disclosure. Is it the amount the dealer makes on one particular deal, is it marketing contribution? Is disclosure a number, a percentage, or the cost of a dinner on a Friday night?”

Moreover, Roelofs queried whether commission disclosure would increase the customer experience. It might well result in no change in customer behaviours, in which case the industry has added cost and new processes to their operations for no useful outcome.

“Or there’s going to be a massive change in behaviour. That doesn’t incentivise brokers to provide a better service because it pushes costs up. It actually encourages the broking industry to commoditise further, which means worse service for the customer. Any blunt instrument will not work, and we don’t understand what it means or the impact,” he added.

After a good-humoured discussion around the benefits of total transparency versus the risks of over regulation, the audience poll at the end of the debate indicated those in favour of full disclosure had dropped ten points, to 45.5%, and those against had risen to 54.5%, meaning the motion was rejected.

The champagne prize for the best audience question (or as Hurwitz put it “who’s thrown the best grenade”) went to broker Tom Perkins from Charles & Dean with a question about why there is a need to disclose commission given that two different brokers could be offering the same product at a standard rate, so why would the customer be concerned about any difference in fee, and was it not also the case that the APR and the overall rate for the deal were more important.

AFC CEO Edward Peck said: “The AFC Big Debate was a new concept for our summer conference, but having seen the quality of the arguments, and the audience’s engagement with what was a lively and well-informed discussion, it will be firmly on our agenda for future events.”