Julian Rose, director, Asset Finance Policy, and a regular commentator on the asset finance industry provides his take on the eventual outcome from the FCA review of motor finance and the impact on the lending market.

There’s a lot of uncertainty about what the FCA will do later this year after it completes the review announced in January. Until then, the regulator has said it will ‘analyse the issues and decide what, if any, further action including legal steps are necessary’.

The effects in the meantime can be seen in Close Brother’s share price, down by over 60% since the FCA’s announcement, and estimates by some analysts of the market-wide costs of compensation to customers at up to £13 billion.

Based in part on my new research, published by Apex Insight, I believe the eventual outcome from this will be far less dramatic than many appear to be assuming. Here’s why.

1. A ‘mass-scale redress scheme’ (as Martin Lewis’s Money Saving Expert website is calling it) would lead to significantly higher prices

The new Apex Insight research confirms that average rates for used car finance have increased since Barclays Partner Finance and Hitachi (now Novuna) left the dealer-introduced finance market.

The research divides the market into ‘low cost’ providers (those charging average rates of up to 10% in February 2024), ‘medium cost’ providers (10% to 30%) and ‘high cost’ providers (rates over 30%).

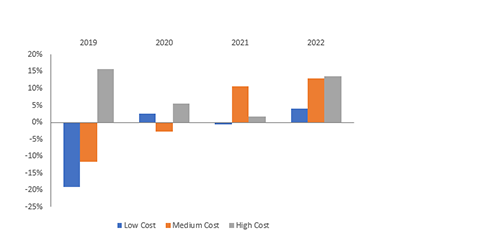

Since 2018, volumes of outstanding loans offered by low cost providers have fallen by 14%, the research finds. The loan books of medium cost providers increased by 8%, and high cost providers were up by 41%.

In real terms – excluding base rate changes – the average rates being paid at portfolio level have increased from 12.3% in 2018 to 13.1% in 2023, with rates for new loans growing faster.

Low cost providers appear to have the greatest exposures to a redress scheme, so there must be a risk that more consumers will lose access to the best rates in the market. Especially with a general election looming, it seems unlikely the Government will want to sit by and let that happen.

Secured Used Car Finance Lending Books % growth rates

Source: Apex Insight Used Car Finance: Market Insight Report 2024

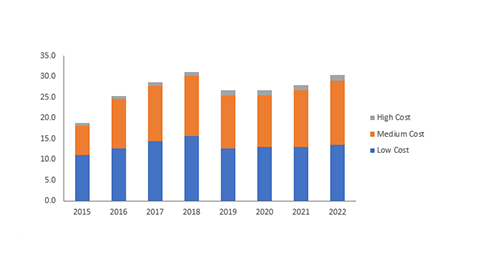

Split of used car secured finance outstanding lending by category of lender (£bn)

Source: Apex Insight Used Car Finance: Market Insight Report 2024

2. The FCA will find that penalising DiC risks promoting alternatives that might be worse for consumers

The more the FCA investigates the market this year, the more complications it will find with isolating DiC as a problem, including:

- Lenders paying fixed commissions that cost more than typical DiC commissions

- Direct lenders paying fees to online search engines and comparison sites for leads where this cost more than the typical commission paid using DiC

- Car dealers, including some of the largest franchised dealers, routinely putting obstacles in the way of consumers selecting cheaper finance through independent brokers, including by refusing to issue invoices or imposing high ‘administration’ fees

3. The FCA will struggle to design a non-arbitrary redress scheme

Even if the FCA still felt it should require a significant redress scheme across the industry, it will need to overcome many practical difficulties.

For example, how would the scheme take account of where DiC commissions were:

- Set at, or towards, the bottom of the range available to the intermediary?

- Set higher than the bottom of the range but where the dealer or broker had to do extra work?

- Set higher than the bottom of the range but where the dealer or broker had higher costs, for example being based in London?

- Set lower than the average cost of providing the broking service?

These, and many other factors, seems bound to rule out a blanket redress scheme.

What can we expect instead?

Instead of a blanket redress scheme for all DiC cases, I expect we will see FCA and FOS eventually publish new guidance on how to assess DiC complaints. Some redress may well be required, but it should be limited to a minority of agreements, and possibly only a small minority, where DiC was used and there is actual evidence of unfair pricing.

Details of Apex Insight’s new report, Used Car Finance: Market Insight Report 2024, available here: https://apex-insight.com/consumer-credit-and-payments/. Julian Rose is Director of Asset Finance Policy

Got a view on the commission crisis you would like to share? Contact lisalaverick@assetfinanceconnect.com